Essential Guide to Bridging Loans

What is a Bridging Loan?

Very simply put, a bridging loan is a short term mortgage with a few important differences as follows…

- Condition of property– Bridging lenders don’t worry about the condition of a property, ultimately all properties have an inherent value and once that is determined by a RICS surveyor, bridging companies will lend accordingly.

- Personal circumstance– Bridging lenders are less hung up on the borrower’s personal situation. If income is low or there have been credit issues, normally a bridging lender will still be comfortable as long as the property being held as security is appropriate and values up correctly.

- Speed– Whereas mortgages take months to arrange, bridging loans take weeks or even just days to complete.

- Interest– Bridging loans are more expensive than mortgages. Most mortgage interest rates are under 5% per annum currently, whereas the minimum interest you will pay on a bridging loan is around 8% pa but often 12-15% and potentially more with associated fees.

- Short term– Mortgages can be taken out for 25 years or more, a bridge can normally only be taken out for up to 12 months, occasionally longer.

Uses

- To buy quickly– If you need to close the deal quickly a bridging loan is the way to do it. Normally you can have terms within hours of an inquiry and cash in the bank within a month if using a good broker and experienced solicitors.

- To realise an uplift in value– If you are buying discounted property or adding value by refurbishment, use a bridge initially and then refinance the property in a few months borrowing against the higher value, leaving less of your own money in the deal.

- To purchase an unmortgageable property– Traditional mortgage lenders will not lend on properties without a functioning bathroom or kitchen so forget it if you are buying a derelict property, a mortgage just won’t cut it.

How much can I borrow?

Generally, up to around 70% of the properties current value or the purchase price, whichever is lower. Some specialist lenders will go to 80% and some will lend based on open market value rather than purchase price, so if you are buying discounted property, occasionally 100% funding is available.

Fees

These can really add up so you must be aware of them early on.

Valuation– Almost always you will have to pay in advance for a Red Book RICS valuation. These can cost anything from around £300.00 to many thousands depending on the size and complexity of the project. The lender will need to instruct the valuation so don’t get one yourself in advance without first checking as you will probably have to pay out again.

Arrangement fee– This is generally around 2% of the loan amount and is deducted from the loan, not paid in advance.

Lender’s legal fees– you have to pay the legal fees of the lender, this will sometimes need to be paid prior to receiving your bridging loan. These fees vary from lender to lender and project to project but are normally upwards of £1000.00

Other fees may include an admin fee, title insurance and an exit fee when you pay the loan back. And sometimes a broker will charge a fee, normally 1% of the loan. So yes, bridging can be expensive but if it allows you to get the deal done, then it’s well worthwhile.

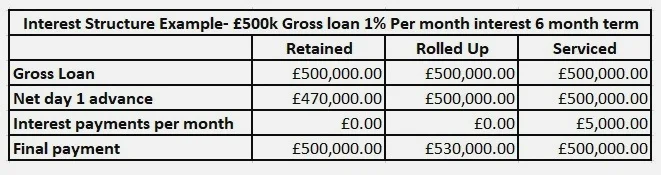

Interest Structure

Retained– Interest is often retained from your loan. So 6 months’ worth of interest could be taken off your loan at the start. This means you do not pay any interest payments during the term of the loan, but you also receive less cash in the bank on day 1.

Rolled Up– This means that the interest for the whole period of the loan is ‘rolled-up’ and payable at the end. This means you get a big cash advance on day 1 and you don’t need to pay interest during the loan term BUT- you have a big payment at the end, so you need to make sure you have plenty of room in the deal to satisfy this.

Serviced Monthly– This means that your interested is payable each month, a bit like a conventional mortgage. It means you get a big cash advance on day 1 but you need to manage your cash flow carefully in order to stay afloat.

*Simplified example to explain interest structures, often other fees will also be deducted from the Gross Loan

The 3 most important considerations for a bridging lender are –

- Security– Is the property in question as it seems, a solid RICS val will soon tell you

- Serviceability– Is the client able to service the loan ie. Pay the monthly interest payments, this is not important for retained or rolled up interest.

- Exit– How does the loan get repaid? Often this will be by refinance onto a long-term mortgage or maybe it is the sale of the completed project. Get this lined up and your lender will have great comfort in the deal.If the lender is happy with the security, serviceability and the exit you will be able to secure competitive terms on your bridging loan.